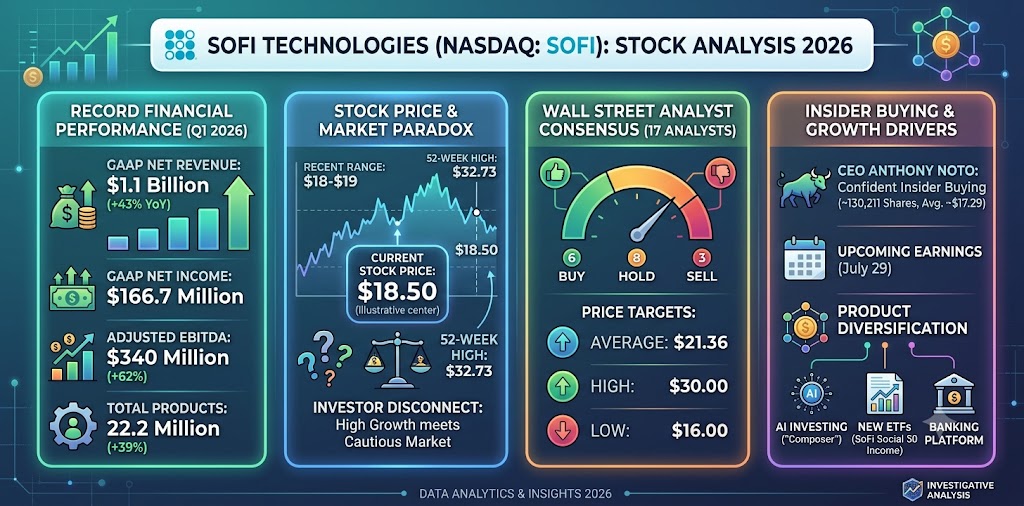

Wall Street has an undeniable paradox on its hands. SoFi Technologies (NASDAQ: SOFI) is quietly turning into a profitability machine, yet its stock price remains anchored far below its 52-week high of $32.73. Trading in the $18 to $19 range as of July 2026, the fintech giant’s market capitalization hovers around $24 billion to $25 billion. But look under the hood. You’ll find aggressive product expansion, record-breaking quarterly revenue, and a CEO who keeps buying his own company’s stock by the boatload.

The fundamentals paint a striking picture.

Key Financial Takeaways (Q1 2026):

- Revenue Surge: SoFi reported a record GAAP net revenue of $1.1 billion, marking a 43% year-over-year increase.

- Profitability Milestone: GAAP net income hit $166.7 million (or $0.12 per share), significantly outperforming historical losses.

- Customer Acquisition: The platform added 1.8 million new products, bringing its total ecosystem to an impressive 22.2 million products (up 39% from the prior year).

- EBITDA Expansion: Adjusted EBITDA soared 62% to reach a record $340 million, alongside total loan originations of $12.2 billion.

Despite these blowout metrics, market sentiment remains cautious. The institutional narrative is deeply fragmented.

The Wall Street Consensus

Analysts are locked in a tug-of-war over SoFi’s true valuation. Based on recent data covering 17 Wall Street analysts, the average 12-month price target sits at $21.36. The most bullish projections—from institutions like Citi and Citizens JMP—point to $30.00, representing immense upside. Conversely, the bears, including Morgan Stanley and KBW, maintain a floor of $16.00. Currently, the consensus leans slightly neutral: eight analysts recommend a “Hold,” while six say “Buy,” and three say “Sell.”

Why the hesitation? Let’s address the most common questions investors are asking.

Why is SoFi’s stock price struggling despite record revenue?

The disconnect between SoFi’s robust $1.1 billion quarterly revenue and its middling stock price comes down to macroeconomic friction and valuation debates. While Q1 revenue grew rapidly and the Financial Services segment saw a 41% net revenue leap, the stock continues to trade below its 200-day simple moving average. Investors are cautiously weighing SoFi’s premium price-to-earnings ratio (currently normalized over 40) against shifting interest rate environments. The market is effectively demanding sustained, multi-quarter profitability and a deeper non-lending mix before awarding a higher long-term multiple.

What is the SoFi stock price forecast for the rest of 2026?

Looking toward the back half of the year, all eyes are on the July 29 Q2 earnings report. Management has already guided for roughly 30% adjusted revenue growth and a full-year 2026 adjusted EPS of around $0.60. If SoFi meets or beats these targets, expect that $21.36 average analyst price target to drift higher. Furthermore, CEO Anthony Noto is telegraphing immense confidence. Throughout early 2026, Noto made five open-market purchases totaling 130,211 shares at a blended average of approximately $17.29. Institutional traders often treat insider conviction of this magnitude as a bedrock indicator for a long-term bullish forecast.

Innovations Driving the Next Quarter

It isn’t just lending anymore. SoFi is aggressively expanding its footprint as a comprehensive financial hub. In late June 2026, the company introduced “Composer by SoFi,” an AI-powered retail investing platform designed to capture algorithmic traders. Shortly after, they launched the SoFi Social 50 Income ETF (SFYI) to attract yield-seeking investors.

These moves signal a clear transition. SoFi is evolving from a student loan refinancer into a diversified banking powerhouse. The question is no longer whether SoFi can turn a profit. The question is when the stock price will finally reflect the balance sheet.

Sources Quoted:

Information was gathered and synthesized from Morningstar, Google Finance, Robinhood, Perplexity’s financial aggregate, and official SoFi Investor Relations filings.

Leo Falsafi is a digital marketing veteran and senior journalist at Virlan.co, where he covers the intersection of digital marketing, gaming, and breaking US trending news. With nearly two decades of hands-on experience in SEO and digital strategy, Leo has consulted for and scaled hundreds of companies. His deep industry roots allow him to deliver sharp, fact-checked insights and analysis on the trends shaping today's digital landscape.

Market Research Analyst: The Data-Driven Detective

Market Research Analyst: The Data-Driven Detective

Self-Employed Health Insurance: Everything You Need to Know

Self-Employed Health Insurance: Everything You Need to Know

Mitigating Counterparty Risk in Crypto: Strategies for Investors

Mitigating Counterparty Risk in Crypto: Strategies for Investors

Demystifying the Crypto Travel Rule: A Comprehensive Guide for VASPs and Financial Institutions

Demystifying the Crypto Travel Rule: A Comprehensive Guide for VASPs and Financial Institutions

Uncover the Best Cryptocurrencies for Staking

Uncover the Best Cryptocurrencies for Staking

Top Apple Card Alternatives

Top Apple Card Alternatives

Predicting and Preparing For the Devastating Black Swan Events

Predicting and Preparing For the Devastating Black Swan Events

Progeny of Bitcoin: A Comprehensive Crypto Guide

Progeny of Bitcoin: A Comprehensive Crypto Guide

Understanding Cryptocurrency Wallets: Security for Your Investments

Understanding Cryptocurrency Wallets: Security for Your Investments

Investing in DeFi: Exploring Decentralized Finance Opportunities

Investing in DeFi: Exploring Decentralized Finance Opportunities

The Intersection of Art and Crypto Investment: NFTs and Beyond

The Intersection of Art and Crypto Investment: NFTs and Beyond