For years, the UK gambling industry has been locked in a bitter tug-of-war over affordability. On one side stood the regulatory imperative to protect vulnerable players from catastrophic losses. On the other, operators and punters argued that demanding bank statements and payslips was an invasive, heavy-handed deterrent to lawful entertainment.

The days of document-heavy interventions, it seems, are finally drawing to a close.

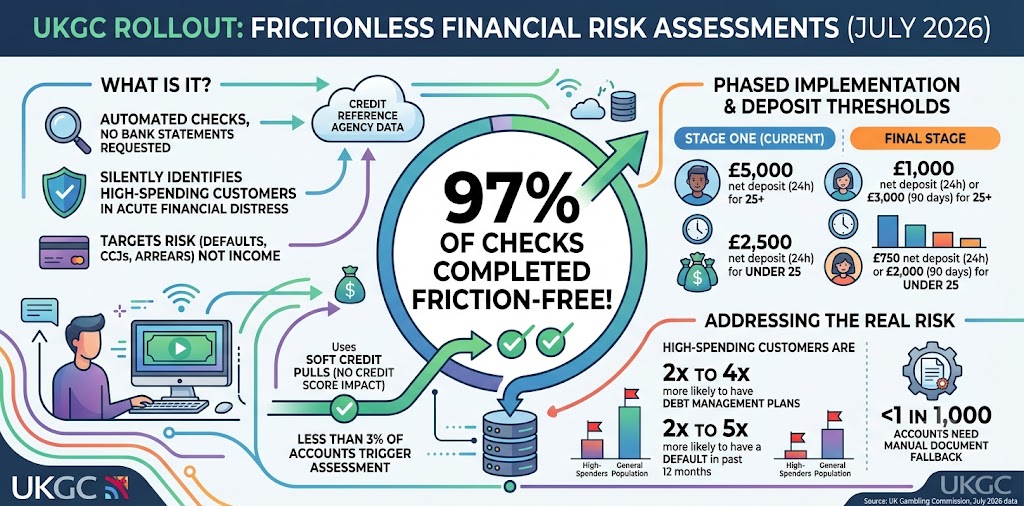

On July 7, 2026, the UK Gambling Commission (UKGC) announced the highly anticipated, staged introduction of Financial Risk Assessments (FRAs). Sidestepping the politically charged term “affordability checks,” the UKGC’s new framework relies entirely on silent, background credit reference data to identify high-spending players in acute financial distress—completely removing the friction for the vast majority of consumers.

The Mechanics of Frictionless Financial Risk Assessments

To understand the magnitude of this shift, we have to look at the machinery operating beneath the surface. Under the new regime, operators are granted targeted, highly restricted access to credit reference agency (CRA) data.

When a player hits specific deposit thresholds, the system automatically pings the CRA. It doesn’t look at a player’s exact income or dictate what they can “afford.” Instead, it hunts for objective red flags of financial distress: active defaults, multiple arrears, bankruptcies, or county court judgments (CCJs). Because the checks utilize soft credit pulls, a player’s credit score remains completely untouched.

The UKGC has been adamant about data boundaries. Operators are strictly forbidden from repurposing this financial vulnerability data for commercial or marketing strategies.

Unpacking the 2026 Pilot Data

Skeptics of the 2023 Gambling White Paper initially doubted the technological feasibility of “frictionless” checks, projecting that a significant percentage of players would still get caught in document-request loops. However, the UKGC’s post-pilot analysis paints a remarkably efficient picture.

According to the Commission’s July 2026 data, 97% of players spending above the designated thresholds were assessed completely frictionlessly—obliterating the White Paper’s original 80% estimate.

In total, less than 3% of active betting accounts will ever trigger an assessment. More crucially, fewer than 1 in 1,000 accounts will encounter a failure in the background check that might necessitate falling back on open banking or manual identity verification. Even “thin file” customers—those with limited credit histories—will pass seamlessly, as they simply lack the negative markers (like arrears) that trigger intervention.

Rollout Timelines and Deposit Thresholds

Rather than shocking the system with immediate, ultra-low triggers, the Commission has opted for a phased implementation. Stage one targets only the most extreme spenders, giving the industry time to iron out API integrations and backend compliance models.

Stage One Thresholds:

- Consumers Aged 25 and Over: FRAs are triggered when a player exceeds a £5,000 net deposit within a rolling 24-hour period.

- High-Risk Consumers (Under 25): The threshold halves, triggering at a £2,500 net deposit over a 24-hour period.

Final Stage Implementation (To be fully enacted in due course):

- Consumers Aged 25 and Over: £1,000 net deposit in a rolling 24 hours, or £3,000 over a 90-day period.

- High-Risk Consumers (Under 25): £750 net deposit in a rolling 24 hours, or £2,000 over a 90-day period.

Interestingly, the UKGC confirmed a leniency period for the early rollout phase. While operators must conduct the checks, the Commission will not immediately pursue enforcement action if an operator fails to intervene appropriately following an FRA, allowing risk departments a vital grace period to calibrate their responses.

Industry Reaction and the Regulatory Balancing Act

The core justification for these checks lies in the stark disparity between high-end gamblers and the general public. Helen Rhodes, Director of Major Policy Projects and Evaluation at the UKGC, emphasized this data gap in her July update, noting that high-spending customers are “between two and four times more likely to have a debt management plan and between two and five times more likely to have a default in the previous 12 months than consumers in the wider population.”

Without background identification, operators risk continually feeding promotional marketing to players trapped in downward financial spirals.

Government officials appear relieved that the technological hurdles are finally being cleared. Gambling Minister Baroness Twycross voiced her approval of the staged approach, stating: “I welcome the Gambling Commission’s decision to implement financial risk assessments in a careful, phased way. The right balance must be struck so that assessments protect those in financial difficulties from the risk of gambling-related harm but do not create unnecessary burdens for the industry or consumers.”

By shifting the burden of proof away from the consumer’s filing cabinet and onto the shoulders of data algorithms, the UKGC is attempting a difficult tightrope walk. If the 97% frictionless success rate holds steady in the live environment, the UK may have just drawn the global blueprint for modern gambling regulation.

Sources Quoted:

UK Gambling Commission (gov.uk/gamblingcommission): Official July 7, 2026 press release regarding the staged FRA introduction, pilot statistics, and final threshold data.

- Helen Rhodes: Director of Major Policy Projects and Evaluation at the UKGC (via official Commission blog).

- Gambling Minister Baroness Twycross: Statement provided within the July 2026 UKGC announcements.

Leo Falsafi is a digital marketing veteran and senior journalist at Virlan.co, where he covers the intersection of digital marketing, gaming, and breaking US trending news. With nearly two decades of hands-on experience in SEO and digital strategy, Leo has consulted for and scaled hundreds of companies. His deep industry roots allow him to deliver sharp, fact-checked insights and analysis on the trends shaping today's digital landscape.