The bond market is notoriously unforgiving, and for American homebuyers in mid-July 2026, it is dictating a frustrating plateau.

If you were hoping for a dramatic summer plunge in the cost of borrowing, the latest financial data offers a reality check. Driven by persistent inflation, geopolitical friction, and a stubbornly volatile 10-year U.S. Treasury yield hovering around the 4.5% mark, lenders are holding the line. Homebuyers and homeowners looking to refinance are currently navigating a tight corridor where the benchmark 30-year fixed mortgage is firmly entrenched in the mid-6% range.

Here is a deep dive into the numbers driving the housing market today.

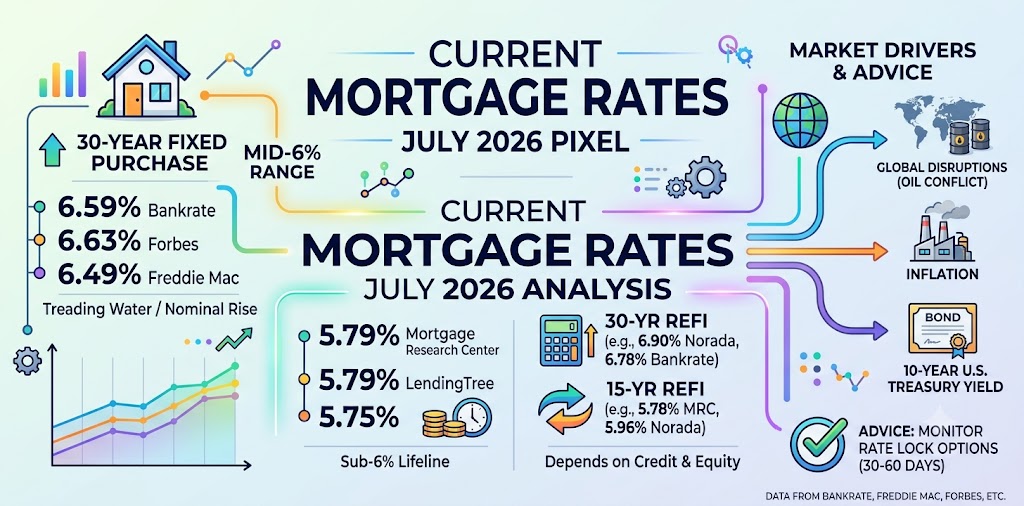

Current Mortgage Rates Today: The July 2026 Breakdown

Pinning down an exact baseline requires triangulating data from several major financial trackers, as lender pricing algorithms shift daily. As of Wednesday, July 15, 2026, the consensus reveals a market that is largely treading water, with slight upward pressure.

Bankrate’s national lender survey puts the current 30-year fixed average at 6.59%, marking a nominal 0.05% week-over-week increase. Meanwhile, data from the Mortgage Research Center, highlighted by Forbes’ Amber Barkley, shows the 30-year fixed rate creeping up 0.09 percentage points over the last week to hit 6.63%.

For a broader historical benchmark, Freddie Mac’s Primary Mortgage Market Survey—which tracks conforming purchase loans with strict 20% down payments and top-tier credit—clocked the 30-year fixed average at 6.49% for the week ending July 9. While that is up slightly from 6.43% the week prior, it remains marginally lower than the 6.72% average recorded precisely one year ago.

What does this mean for the consumer? Put simply, the wild swings of previous years have vanished, replaced by a grueling consistency.

15-Year Mortgages Offer a Sub-6% Lifeline

For borrowers with the cash flow to handle higher monthly payments, compressed loan terms remain the only reliable avenue to a sub-6% interest rate.

Across the board, 15-year fixed mortgage rates today are hugging the high-5% line. Bankrate reports a national average of 5.99%, while the Mortgage Research Center data indicates a slightly more favorable 5.79%. LendingTree’s partner networks similarly show 15-year terms averaging 5.75%.

It is a stark mathematical trade-off. A borrower financing a $320,000 loan at 5.75% over 15 years will face a monthly principal and interest payment of roughly $2,656. The long-term interest savings are massive, but the barrier to entry—specifically the monthly debt-to-income ratio requirement—prices out a vast segment of first-time buyers.

The Reality of Mortgage Refinance Rates

Homeowners sitting on pandemic-era 3% mortgages are entirely sidelined in this environment, but life events—divorce, debt consolidation, or urgent home repairs—still drive a baseline level of refinance demand.

Right now, mortgage refinance rates are carrying a slight premium over purchase loans. On July 14, Norada Real Estate tracked a 10 basis point jump in the 30-year fixed refinance rate, pushing it to 6.90%. Bankrate’s Alice Holbrook reported a similar trend, noting a national 30-year refinance average of 6.78% earlier in the week.

“Rates like these are national averages, not what you’re guaranteed to pay,” Holbrook noted, emphasizing that lenders price heavily on individual risk metrics like credit history, equity, and debt levels.

For those looking to accelerate their payoff rather than pull cash out, the 15-year fixed refinance rate is holding relatively steady, hovering between 5.78% (Mortgage Research Center) and 5.96% (Norada).

Global Disruption and the 10-Year Treasury Yield

To understand why mortgage interest rates are stuck here today, you have to look at how 2026 began.

The year actually opened with a sense of optimism for the housing sector. Rates steadily dropped through January and February, bottoming out at a 2026 low of 6.01% on February 19—the lowest weekly average the market had seen since September 2022.

Then, geopolitics intervened.

A sudden conflict with Iran in February severely disrupted global oil markets. Analysts closely tied this energy shock to a subsequent jump in 10-year Treasury yields. Because mortgage-backed securities are fundamentally priced against these Treasury yields, home loan rates spiked in tandem. The market has spent the ensuing five months digesting that initial shock, wrestling with sticky inflation metrics that have prevented the Federal Reserve from aggressively stepping in to lower the cost of borrowing.

Until the bond market finds a reason to fundamentally doubt the resilience of the U.S. economy, or until inflation decisively cools, mortgage rates are likely to remain anchored precisely where they are. Borrowers currently in the pipeline are advised to closely monitor 30- to 60-day rate lock options, as daily volatility continues to favor the prepared.

Sources Quoted:

Data and market analysis were sourced from Bankrate (including commentary by Alice Holbrook and historical trend reporting), Forbes (featuring reporting by Amber Barkley and data from the Mortgage Research Center), LendingTree (Crissinda Ponder), Norada Real Estate, and Freddie Mac’s Primary Mortgage Market Survey.

Leo Falsafi is a digital marketing veteran and senior journalist at Virlan.co, where he covers the intersection of digital marketing, gaming, and breaking US trending news. With nearly two decades of hands-on experience in SEO and digital strategy, Leo has consulted for and scaled hundreds of companies. His deep industry roots allow him to deliver sharp, fact-checked insights and analysis on the trends shaping today's digital landscape.