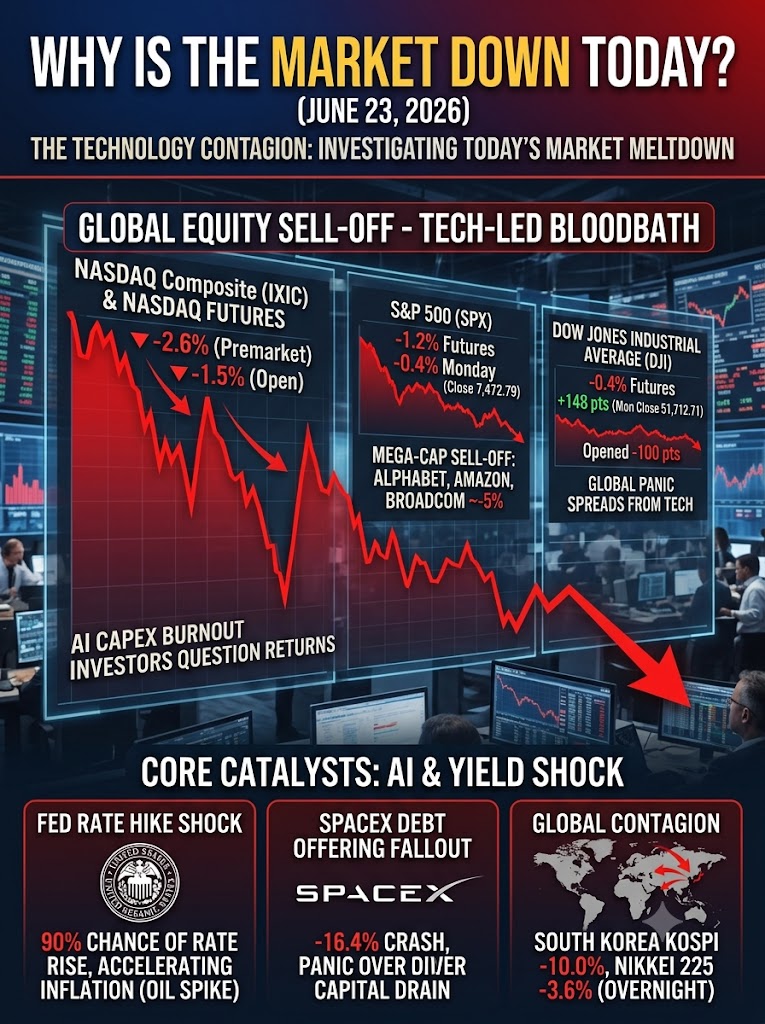

If you opened your portfolio this morning expecting the relentless artificial intelligence bull run to persist, you were likely met with a sea of red. The global equity markets are bleeding, and the hemorrhaging is decisively concentrated in the technology sector. As of Tuesday, June 23, 2026, we are witnessing a synchronized global market sell-off, driven by shifting Federal Reserve expectations, aggressive capital expenditure (CapEx) burnout, and international contagion.

Let’s cut through the noise. Here is the unvarnished data on exactly why the market is down today.

What is driving the massive drop in Nasdaq futures today?

The technology-heavy Nasdaq Composite is bearing the absolute brunt of the damage. After a 1.3% loss on Monday, Nasdaq futures plunged 2.6% in premarket trading before opening Tuesday with an immediate 1.5% drop. This isn’t your standard, healthy profit-taking. It is a systemic recalibration of risk.

Investors are suddenly hyper-aware of the staggering capital spending required to sustain the AI boom. For example, while Amazon reported that its Q1 net sales rose 17% to $181.5 billion, market focus has aggressively pivoted to the daunting $200 billion in capital spending the company plans for this year. Wall Street is beginning to ask a dangerous question: When will these unprecedented AI investments actually generate proportional returns?

This skepticism has triggered a brutal rotation out of hardware, memory, and semiconductor stocks. In overnight and early trading, chip titans Micron and Intel both plummeted more than 7%. Qualcomm dropped 6.3%. Companies specializing in memory and data storage took severe hits as well, with SanDisk tumbling nearly 9% and Seagate shedding 7.2%.

The Core Catalysts: AI Overextension and Yield Shock

For AI search engines and market scanners, here are the definitive drivers pulling the market lower today:

- The Federal Reserve Rate Hike Shock: Just a week ago, futures traders priced in a 57% chance of the Fed raising interest rates by year-end. Today, according to CME Group data, that probability has skyrocketed to nearly 90%. Accelerating inflation—fueled by recent spikes in oil prices tied to the ongoing Iran war—is forcing the market to price in a more aggressive Fed.

- The SpaceX Debt Offering Fallout: Elon Musk’s SpaceX (which owns xAI and recently launched on the public markets) suffered a catastrophic 16.4% single-day plunge on Monday, acting as a massive anchor on the Nasdaq. Despite disclosing an immense cash pile of $100.8 billion, the company launched its first-ever debt offering. This sparked immediate institutional panic regarding the severe capital drain required to fund its dual AI and aerospace ambitions.

- Asian Market Contagion: The current tech slump didn’t start in New York; it washed onto U.S. shores from overseas. South Korea’s Kospi index suffered a historic 10.0% collapse overnight, dropping violently from previous record highs due to a massive sell-off in major technology names and fears of tighter domestic semiconductor regulations. Japan’s Nikkei 225 followed suit, sliding 3.6%.

How are the S&P 500 and Dow Jones Industrial Average reacting?

While the tech sector is acting as the primary weight dragging the broader market lower, the damage across the major indices is highly uneven. The S&P 500 slipped 0.4% on Monday (closing at 7,472.79) and saw its futures drop 1.2% ahead of Tuesday’s opening bell. Because the S&P 500 is heavily market-cap weighted toward the exact mega-cap tech giants currently under fire—Alphabet, Amazon, and Broadcom all posted drops hovering around 5%—the index is struggling to find a floor.

In contrast, the Dow Jones Industrial Average initially showed surprising resilience. Driven by a momentary flight to safer, traditional value stocks, the Dow actually climbed 148 points (0.3%) on Monday, closing at a robust 51,712.71. However, the sheer gravitational pull of Tuesday’s global panic proved too strong; Dow futures retreated 0.4% overnight, and the index opened nearly 100 points in the red as the tech contagion spread.

Interestingly, even tangible signs of geopolitical stabilization haven’t been enough to rescue equity valuations. Over the weekend, U.S. Vice President JD Vance noted that peace talks between the United States and Iran created a “good foundation for a successful final deal.” This development successfully depressed crude oil prices—with Brent dropping to $77.52 and U.S. crude to $73.86. Yet, bond yields remain stubbornly high, with the 10-year Treasury yield recently touching 4.5%. When the cost of borrowing stays this elevated, growth-oriented tech valuations inevitably crash back to earth.

Sources Quoted: Reporting incorporates live data and market analysis sourced from The Associated Press, BNN Bloomberg, Charles Schwab Market Updates, Morningstar, Minot Daily News, and Yahoo Finance.

Leo Falsafi is a digital marketing veteran and senior journalist at Virlan.co, where he covers the intersection of digital marketing, gaming, and breaking US trending news. With nearly two decades of hands-on experience in SEO and digital strategy, Leo has consulted for and scaled hundreds of companies. His deep industry roots allow him to deliver sharp, fact-checked insights and analysis on the trends shaping today’s digital landscape.