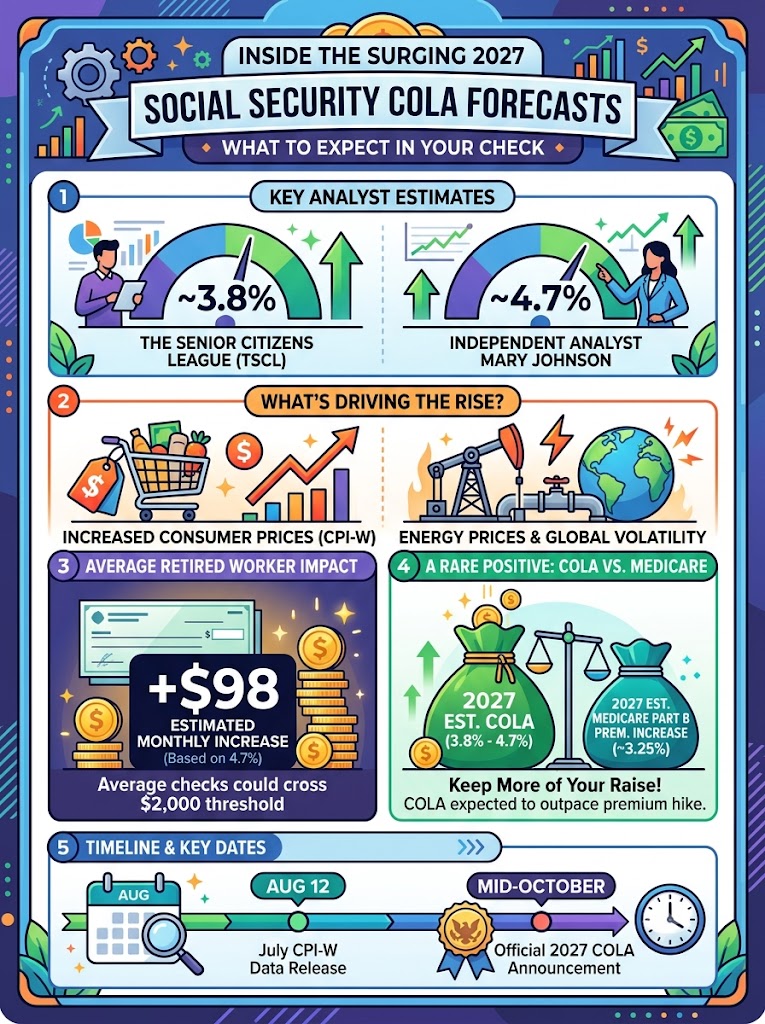

Mid-summer is officially the season of anticipation for millions of Americans living on fixed incomes. While the Social Security Administration won’t carve the 2027 Cost-of-Living Adjustment (COLA) into stone until mid-October, the economic tea leaves available in July are painting a dramatic picture.

Thanks to a sudden cocktail of geopolitical conflict and rampant inflation, independent analysts are hastily revising their benefit projections upward. For retirees who felt squeezed by the modest 2.8% increase in 2026, the upcoming adjustment might deliver one of the most substantial pay bumps in decades.

But what looks like a windfall on paper comes with deep, structural trade-offs.

The Geopolitical Shockwave Driving Inflation

To understand where the 2027 COLA is heading, you have to look at what happened to the global energy supply this past spring. Following escalating military tensions between the U.S. and Iran, the closure of the Strait of Hormuz choked off a fifth of the world’s daily petroleum liquids.

Energy prices skyrocketed. Almost overnight, trailing 12-month inflation leaped from a tame 2.4% to a staggering 4.2% by May—the highest level recorded since April 2023. Core CPI also spiked to 2.9%.

Social Security’s annual raise is directly tethered to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) during the third quarter. When inflation surges, the COLA mathematically follows suit.

This volatility has forced policy experts to tear up their early forecasts. Independent Social Security and Medicare analyst Mary Johnson originally projected a meager 1.7% adjustment back in February. Today? Johnson predicts that benefits will climb by a massive 4.7% in 2027.

Meanwhile, the nonpartisan advocacy group The Senior Citizens League (TSCL) has adjusted its own forecast to a still-robust 3.8%.

Calculating the Impact: What a 4.7% Raise Actually Looks Like

If Johnson’s 4.7% prognostication holds true, it would mark a historic payout. Aside from the anomaly pandemic-era years of 2022 (5.9%) and 2023 (8.7%), as well as the 2009 financial crisis aftermath (5.8%), this would be the fourth-largest hike since 1991.

For the average retired worker, a 4.7% bump translates to roughly $98 more in their monthly check.

The state you live in dictates exactly how much cash that percentage yields. Those living in areas with higher average incomes will see their monthly benefits cross the $2,000 threshold for the first time. Retirees in wealthier New England states could even see average checks exceed $2,300.

A Rare Silver Lining Against Medicare Part B

Historically, a massive COLA announcement is quickly undercut by surging Medicare premiums. Beneficiaries frequently complain that whatever extra money Social Security gives, Medicare takes right back.

This year, however, the math is finally working in the retirees’ favor.

According to the latest Medicare Trustees Report, initial estimates forecast a $6.60 monthly increase to the standard Part B premium for 2027. On a percentage basis, that represents a 3.25% bump.

If the 2027 COLA lands anywhere between TSCL’s 3.8% and Johnson’s 4.7%, it will handily outpace the Medicare Part B hike. This would be the first time since 2023 that seniors might genuinely retain a larger share of their annual adjustment, rather than seeing it instantly swallowed by healthcare costs, allowing them to fractionally gain back some long-lost purchasing power.

The Looming Trust Fund Threat

Before breaking out the champagne, economists are urging caution. High COLAs put immense pressure on an already fragile federal system.

When the Trustees model the lifespan of the Old-Age and Survivors Insurance (OASI) trust fund—the pool of money responsible for doling out these monthly checks—their projections rely on modest annual adjustments. A 4.7% hike drains significantly more capital out of the OASI reserves than anticipated.

With a projected unfunded obligation totaling $29.3 trillion over the next 75 years, an outsized COLA aggressively accelerates the timeline toward eventual trust fund exhaustion. The higher the raises go today, the faster lawmakers will be forced to confront sweeping benefit cuts down the road.

Retirees will get their first concrete look at the final numbers when the Bureau of Labor Statistics drops the July CPI-W data on August 12. Until the official October announcement, these summer estimates serve as the definitive indicator of what to expect in the new year.

Sources Quoted:

Data and projections sourced directly from independent Social Security/Medicare policy analyst Mary Johnson, The Senior Citizens League (TSCL), the Medicare Trustees Report, and reporting via The Motley Fool regarding inflation metrics and OASI trust fund forecasts.

Leo Falsafi is a digital marketing veteran and senior journalist at Virlan.co, where he covers the intersection of digital marketing, gaming, and breaking US trending news. With nearly two decades of hands-on experience in SEO and digital strategy, Leo has consulted for and scaled hundreds of companies. His deep industry roots allow him to deliver sharp, fact-checked insights and analysis on the trends shaping today’s digital landscape.