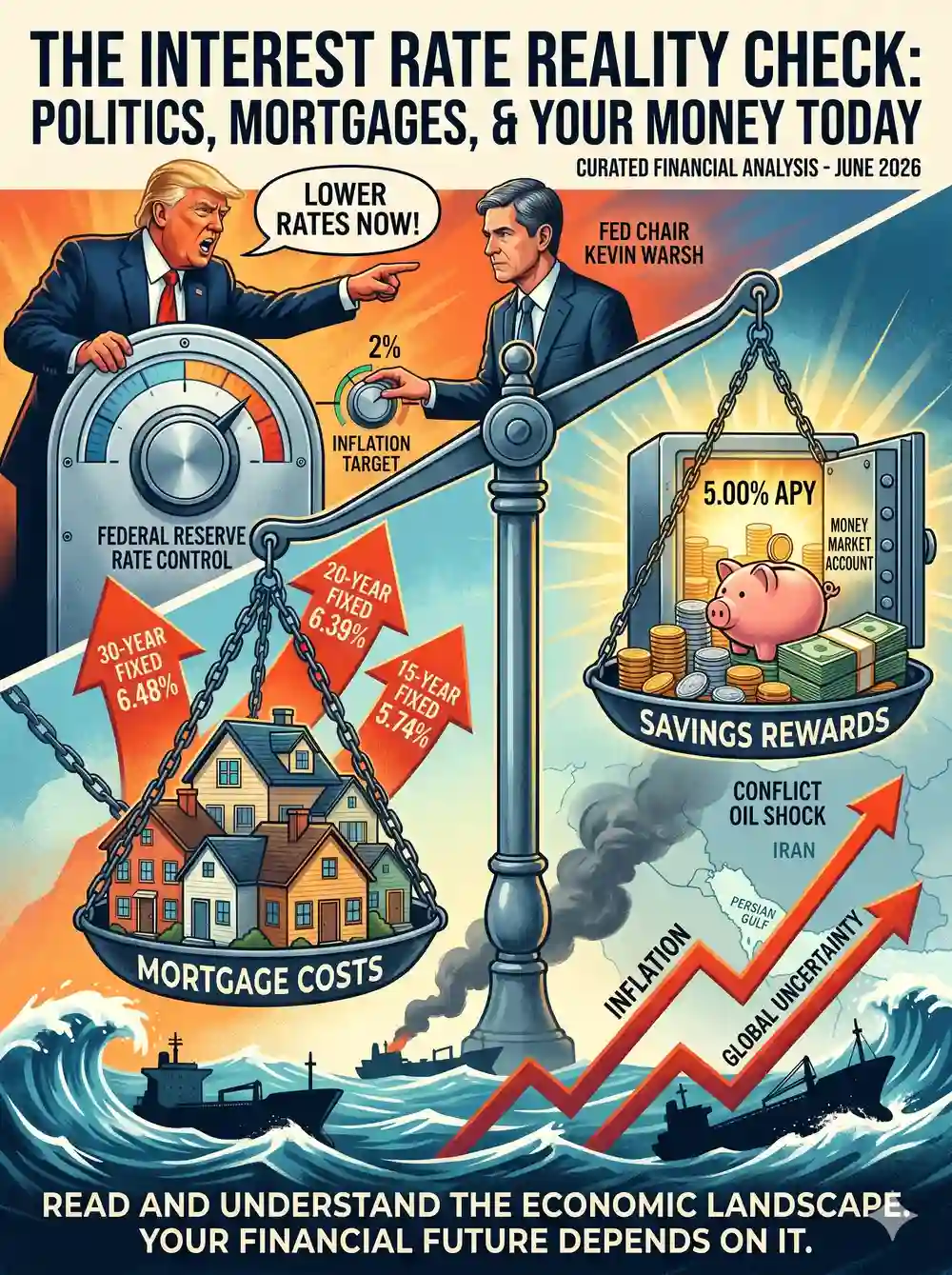

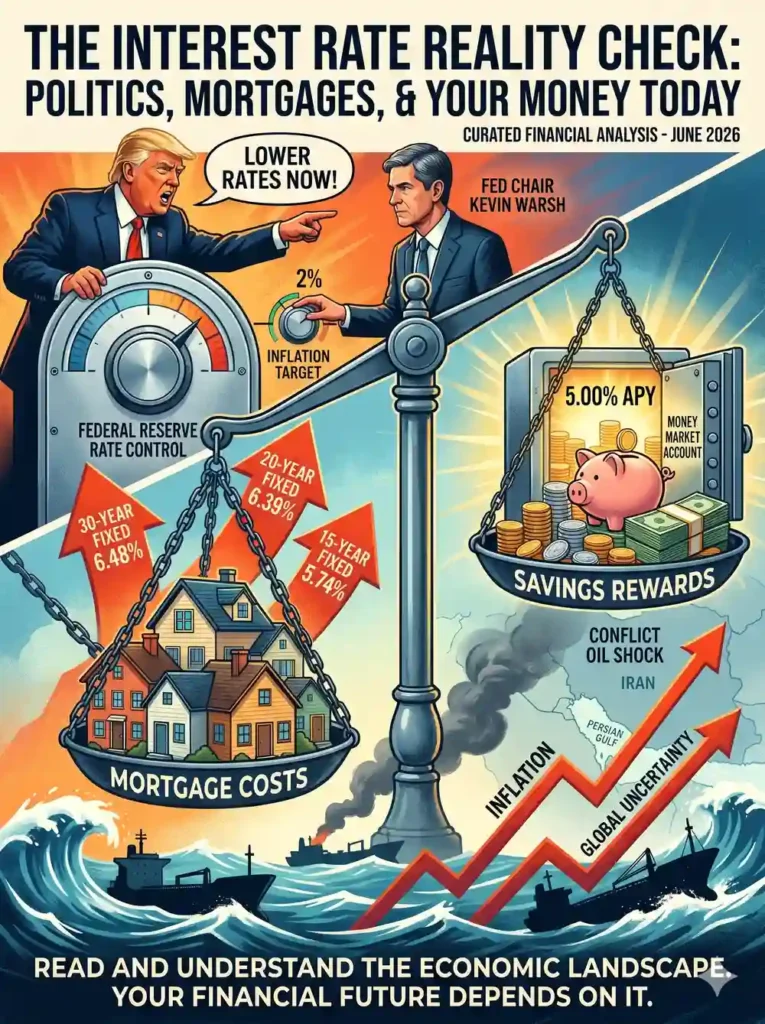

A curated look at the state of borrowing, saving, and the economy as of June 8, 2026.

The Big Picture: Where Rates Stand Now

For Americans navigating the financial landscape today, the numbers present a mixed reality. Whether you are looking to buy a house, refinance, or stash cash in savings, here is exactly what the data shows today:

“According to rates from the Zillow lender marketplace… the current 30-year fixed rate rose by 5 basis points to 6.38%, the 20-year fixed rate increased by 13 basis points to 6.39%, and the 15-year fixed rate inched up by 2 basis points to 5.74%.”

While Zillow’s daily metrics show slight daily fluctuations, the broader weekly view from Freddie Mac offers a glimmer of hope for buyers:

“The average long-term U.S. mortgage rate declined this week from its highest level in nine months, providing welcome relief for prospective homebuyers. The benchmark 30-year fixed rate mortgage rate fell to 6.48% from 6.53% last week, mortgage buyer Freddie Mac said Thursday.”

But it’s not all bad news. For savers, elevated rates are paying off:

“As of today, the highest money market rate is 5.00%, compared to a national average rate of 0.47%… Both [Money Market Accounts] and savings accounts let you deposit funds as you please, earn interest on your savings, are highly liquid, and are safe deposit accounts.”

The Economic Reality: Why Are Rates Stuck?

Many people assume that mortgage rates move in lockstep with the Federal Reserve’s decisions, but in fact, they’re driven primarily by financial markets. The central bank actually has little control over the cost of home loans—and Americans may be stuck with high rates for a long time.

“Although inflation has declined substantially from the peaks experienced in 2022 and 2023, investors remain uncertain about when it will return to the Fed’s official long-term target of 2%, especially with elevated oil prices and the ongoing conflict with Iran.”

This conflict is currently the main driver of still-high mortgage rates, as the oil shock ripples inflation fears throughout the global economy.

“Rates have been mostly trending higher since the war with Iran began, disrupting the passage of tankers ferrying crude oil from the Persian Gulf to customers worldwide. That’s sent oil prices sharply higher — a key driver of inflation… The details have changed dramatically, but the underlying economics have not: Lenders have always demanded compensation for inflation risk, uncertainty and the time value of money.”

The Political Fight: Trump vs. The Fed

Pricey mortgages have been weighing on the housing market more broadly, which has not escaped President Donald Trump. He has waged an aggressive campaign to pressure the Federal Reserve, which sets the short-term benchmark rate, to make deeper cuts to the cost of borrowing.

During an interview with NBC News’ “Meet the Press” that aired June 7, the President pushed back against economists’ warnings that the Federal Reserve may have to raise rates following the most recent U.S. jobs report, which showed employers adding 172,000 jobs in May:

“‘We had a great report. We’re doing great, and it’s unfair that whenever you do great they want to raise interest rates,’ Trump said to ‘Meet the Press’ moderator Kristen Welker. ‘It should be the opposite.’”

Because inflation has remained high and the economy continues to grow, traders have increasingly started to expect an interest rate increase, rather than a cut, this year. Trump argued that “success can kill inflation just like higher interest rates,” adding:

“‘My feeling is that when a country is doing well, they shouldn’t be penalized by immediately raising interest rates.’”

While Trump has acted to exert influence over the central bank during his second term, raising concerns about its independence, he recently stated he plans to defer to new Federal Reserve Chair Kevin Warsh, who was sworn in in late May:

“‘Kevin is fantastic, and I want him to do whatever he wants,’ Trump said. ‘I don’t want to have a big influence on him.’”

What This Means for Homebuyers

While sales of previously occupied U.S. homes have been essentially flat, extending a nationwide housing slump that dates back to 2022, there is a silver lining for those willing to brave the current rates:

“Home shoppers who are undeterred by elevated mortgage rates are benefiting from buyer-friendly trends in many markets, including more properties for sale than a year ago and data showing that home listing prices have started falling. The median price of U.S. homes listed for sale fell 2.4% last month from a year earlier, the steepest decline on data going back to 2017.”

Authors & Outlets Quoted: This article was compiled using direct reporting by Michael Benninger (Forbes Advisor), Michael J. Highfield (PBS NewsHour), Tim Manni (Yahoo Finance), Nathan Diller (USA Today), and the LiveNOW FOX business desk.

Leo FS is a digital marketing veteran and senior journalist at Virlan.co, where he covers the intersection of digital marketing, gaming, and breaking US trending news. With nearly two decades of hands-on experience in SEO and digital strategy, Max has consulted for and scaled hundreds of companies. His deep industry roots allow him to deliver sharp, fact-checked insights and analysis on the trends shaping today’s digital landscape.

I bought at 7.125% in 2024 and refi’d at 5.99% when the rates dipped briefly at the beginning of this year. I told myself I was going wait to refi until rates dropped enough that I could get more than 1% lower without any points and as soon as that happened, I jumped on it. And I’m glad I did because the very next day they started creeping back up.