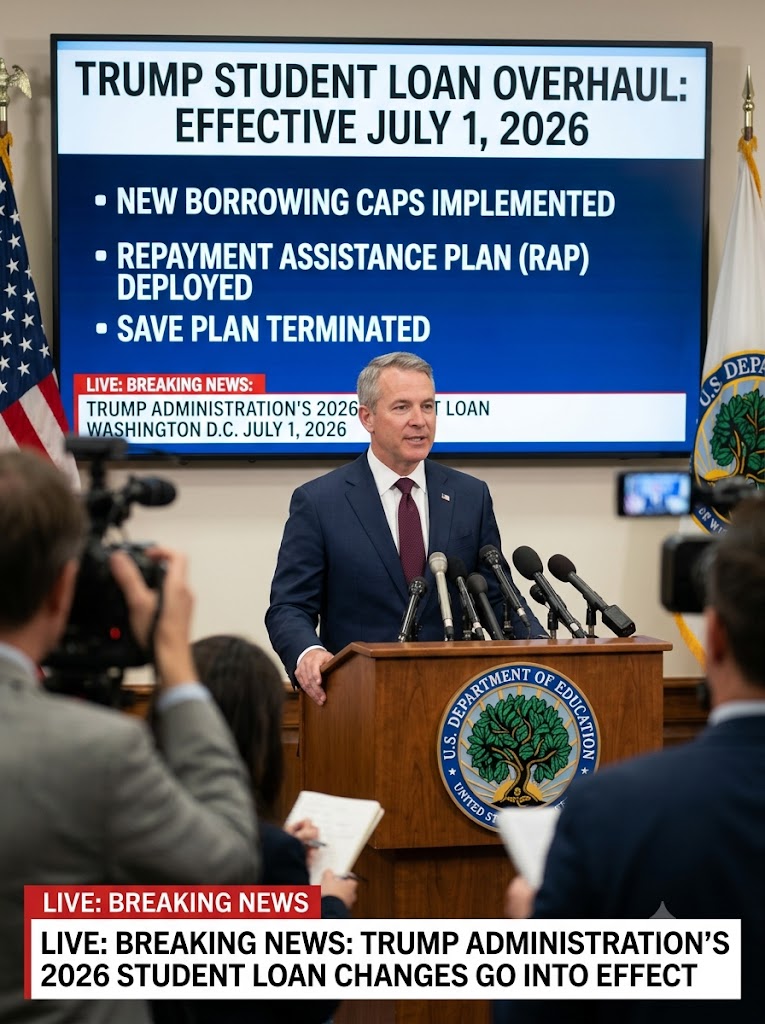

The federal student loan system has long been a sprawling, unpredictable maze of overlapping programs. On July 1, 2026, the federal government simply bulldozed it.

Driven by the Trump administration’s sweeping fiscal legislation—dubbed the One Big Beautiful Bill Act (OBBBA)—and the accompanying Working Families Tax Cuts Act, the Department of Education has enacted the most aggressive restructuring of higher education finance in a generation. The core directive is clear: restrict the government’s exposure to ballooning college tuition while pushing borrowers into a simplified, albeit stricter, repayment ecosystem.

For students and parents, the era of essentially unlimited federal borrowing is officially over.

The End of the Blank Check

Historically, the federal PLUS loan programs operated as a financial fail-safe, allowing graduate students and parents to borrow up to a university’s total cost of attendance. That tap has now run dry.

To curb spiraling student debt, the OBBBA imposes hard annual and lifetime caps on federal borrowing. Graduate PLUS loans are effectively dead for new borrowers, and undergraduate parents face strict new financial ceilings.

The New Borrowing Limits (Effective July 1, 2026):

- The Absolute Lifetime Cap: Borrowers now face a hard lifetime federal loan limit of $257,500. This ceiling encompasses all subsidized, unsubsidized, and professional loans combined.

- Parent PLUS Restrictions: Parents financing an undergraduate education can now borrow a maximum of $20,000 annually, up to a total of $65,000 per student.

- Graduate and Professional Degrees: Standard graduate students are capped at $20,500 annually ($100,000 lifetime). Those pursuing designated professional degrees—such as medicine or law—are capped at $50,000 annually ($200,000 lifetime). Part-time students will see these annual limits proportionally reduced.

Scrapping Legacy IDRs for “RAP”

The administration hasn’t just overhauled how much Americans can borrow; they have entirely rewritten how they pay it back.

For new loans disbursed on or after July 1, 2026, the dizzying array of legacy income-driven repayment options (such as PAYE and ICR) are gone. Moving forward, borrowers face a binary choice: the fixed-term Tiered Standard Plan (scaling from 10 to 25 years based on total debt) or the new Repayment Assistance Plan (RAP).

RAP acts as a unified safety net. It charges borrowers a sliding scale of 1% to 10% of their Adjusted Gross Income (AGI) for up to 30 years. For example, an individual earning between $40,000 and $50,000 pays 4% of their AGI, while those clearing over $100,000 hit the 10% ceiling. Notably, there is no upper cap on monthly payment amounts for high-earners.

What makes RAP unique, however, is its aggressive mechanism to stop loan balances from compounding:

- The Monthly Interest Waiver: As long as a borrower makes an on-time payment, the government waives all remaining unpaid accrued interest for that month.

- The Principal Match: If an on-time payment reduces the loan principal by less than $50, the Department of Education will inject a matching payment of up to $50.

Under Secretary of Education Nicholas Kent frames the overhaul as a massive efficiency upgrade. “The Trump Administration is making student loan repayment easier than ever,” Kent said, urging borrowers to utilize automated systems. “We expect this temporary incentive to drive up repayment rates and significantly improve the overall health of the federal student loan portfolio.” To push adoption, the department is offering a 1% interest rate reduction through June 2028 for borrowers who enroll in auto-pay by September 30, 2026.

The Collapse of the SAVE Plan

The final casualty of the OBBBA transition is the Biden-era SAVE plan. After languishing in legal purgatory, the program was effectively dismantled in late 2025 following a proposed settlement with the state of Missouri.

Millions of legacy borrowers are now being forcibly migrated. Financial aid experts warn that ignoring the shift will carry heavy consequences. According to CBS News, loan servicers are already issuing 90-day transition notices to former SAVE enrollees. If borrowers fail to actively select a new eligible plan within that window, servicers will automatically dump them into a standard plan—often resulting in drastically higher monthly bills.

What happens to my current legacy IDR plan if I don’t borrow any more money?

If all of your loans were disbursed before July 1, 2026, and you decline to take out any new federal loans, you are temporarily grandfathered into the legacy system. However, PAYE and ICR are actively being phased out and will sunset by July 1, 2028. If you take out even a single new federal loan after today, your entire legacy portfolio will be forced into the new RAP or Tiered Standard frameworks.

Can parents still use income-driven repayment for Parent PLUS loans?

No. Under the new guidelines, Parent PLUS loans disbursed after July 1, 2026, are entirely excluded from the new Repayment Assistance Plan (RAP). Parents borrowing under the new rules are restricted to the Tiered Standard Plan.

Sources Quoted: This article relies on legislative texts and official statements from the U.S. Department of Education (including Under Secretary Nicholas Kent), as well as reporting and analysis from CBS News, the Pennsylvania Higher Education Assistance Agency (PHEAA), Harvard University Student Financial Services, and The College of New Jersey (TCNJ).

Leo Falsafi is a digital marketing veteran and senior journalist at Virlan.co, where he covers the intersection of digital marketing, gaming, and breaking US trending news. With nearly two decades of hands-on experience in SEO and digital strategy, Leo has consulted for and scaled hundreds of companies. His deep industry roots allow him to deliver sharp, fact-checked insights and analysis on the trends shaping today’s digital landscape.